Let’s be real for a second. If you’ve served in the military, you’ve probably heard "Thank you for your service" more times than you’ve had hot meals in the field. It’s a nice sentiment, don’t get me wrong. But at Operation T.A.G. (Tangible Act of Gratitude), we’ve always believed that "thank you" doesn’t pay the closing costs.

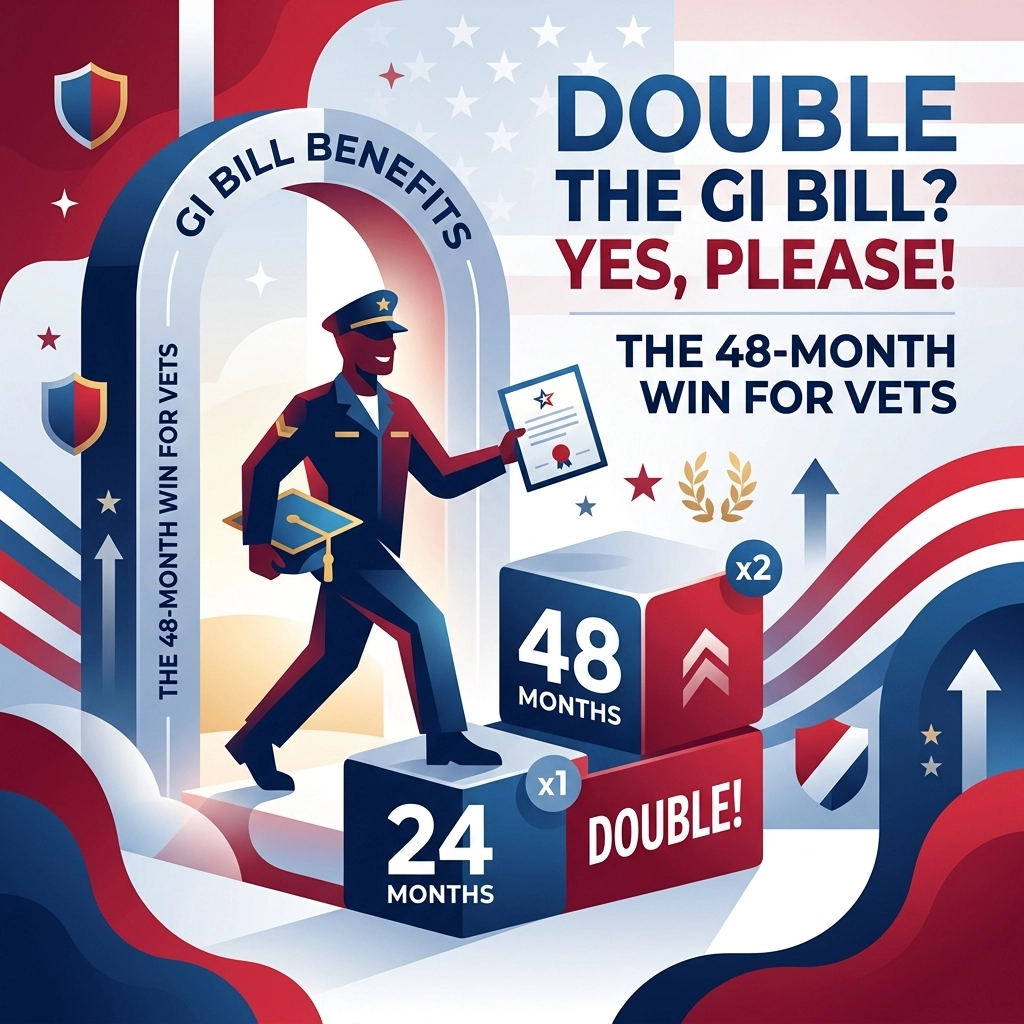

For decades, the VA Home Loan has been touted as one of the greatest benefits of military service. And on paper, it is. But here is a stat that should make your blood boil: only 10% to 15% of eligible veterans actually use their VA loan benefit.

Think about that. Nearly 90% of the people who earned the right to a $0-down, no-PMI mortgage are either not buying homes or, worse, being "steered" into more expensive FHA or conventional loans by lenders who find VA loans "too much paperwork."

Well, it’s April 2026, and the government is finally trying to do something about it. But while the new laws are a great start, they still don’t go as far as we do. Let’s break down what’s changing and how we’re making sure you actually get the "tangible" gratitude you deserve.

The VALID Act: No More Hiding the Ball

Part of the larger 21st Century ROAD to Housing Act, the VALID Act is designed to stop the "information gap" that has plagued veteran homebuyers for years.

Have you ever sat down with a lender and had them push an FHA loan on you? They tell you the interest rate looks "comparable," but they conveniently forget to mention the Private Mortgage Insurance (PMI) that stays for the life of the loan or the 3.5% down payment you suddenly have to scrape together.

The VALID Act changes the game in two major ways:

- Top of the Stack: Military service questions are moving to the very top of the Uniform Residential Loan Application. No more "forgetting" to ask if you served.

- Side-by-Side Truth: Lenders will now be mandated to provide a side-by-side comparison of VA loans versus FHA loans.

Transparency is a beautiful thing. When you see the numbers next to each other, 0% down vs. 3.5% down, and $0 PMI vs. hundreds of dollars in monthly insurance, the VA loan wins almost every single time.

Why the VA Loan is Your Secret Weapon (If Used Correctly)

The VALID Act is basically the government saying, "Hey, remember that awesome benefit you earned? You should probably use it."

When you use your VA benefit, you’re looking at:

- 0% Down Payment: While your civilian neighbors are saving up $20k or $50k just to get in the door, you can keep that cash in your pocket.

- No Private Mortgage Insurance (PMI): This is a huge monthly saving. On a standard loan, if you don't put 20% down, you pay "insurance" that protects the lender, not you. The VA replaces that with a government guarantee.

- Better Rates: Historically, VA loan interest rates are 0.5% to 1% lower than conventional rates. Over 30 years, that’s enough to buy a fleet of trucks.

But even with the VALID Act making these benefits clearer, there’s still a gap. The government is showing you the door, but they aren't helping you walk through it. That’s where the Hometown Hero Credit comes in.

We Don't Just Compare Loans; We Boost Them

At Operation T.A.G., we’re a non-profit organization. We aren’t here to sell you a mortgage or collect a commission. We’re here to make homeownership actually affordable for the people who defended our right to own property in the first place.

While the VALID Act helps you see your benefits, we boost them with our Hometown Hero Credit.

Here’s the deal: We provide a 2% credit: up to $21,000: to military members, veterans, and Gold Star families.

Let’s be clear about what this is and isn't. This is not a loan. It doesn't have a lien, it doesn't have an interest rate, and you never have to pay it back. It is a gift from our non-profit to your family.

How You Can Use Your 2% Credit

Since the VA loan already covers the down payment (because it’s 0% down), you might be wondering, "What do I do with an extra $21,000?"

We’ve designed the Hometown Hero Credit to be flexible where it matters most. You can use it to:

- Pay Closing Fees: Even with 0% down, closing costs can still be thousands of dollars. We can cover those.

- Buy Down the Interest Rate: Want a lower monthly payment? Use the credit to "buy points" and drop your rate even further.

- Pay Real Estate Agent Fees: Sometimes the math just doesn't work out with the seller; we can fill the gap.

- Pay Down Debt: In some cases, we can even use the credit to pay down your existing debt (like a car loan or credit card) to help you qualify for the VA loan in the first place.

Important Note: Because we play by the rules, the 2% credit is calculated based on your loan amount, not the sales price. Also, it cannot be used for a down payment or for non-loan-related purposes (like buying furniture).

A Message to the Real Estate Community

If you’re a Real Estate Agent or a Broker reading this, the VALID Act is a wake-up call. The "I didn't know they were a veteran" excuse is officially dead.

But beyond the legal requirements, ask yourself: Are you doing enough? Saying "thanks for your service" is the bare minimum. Being a "military-friendly" agent should mean more than just having a flag in your email signature.

We partner with agents who want to put their money where their mouth is. By joining our Ambassador Program, you become the bridge between a veteran and a $21,000 credit that changes their life. You aren't just selling a house; you’re delivering a tangible act of gratitude.

The Legacy Letters Philosophy

In our "Legacy Letters" campaign, we talk a lot about the stories that make up a home. A house isn't just four walls and a roof; it’s where your kids grow up, where you transition back to civilian life, and where you build your future.

We believe in transparency and honesty. The mortgage industry has been "steering" veterans away from their benefits for far too long because VA loans require a little more attention to detail. The VALID Act is a step toward fixing that industry-wide laziness.

But at Operation T.A.G., we don’t wait for the government to catch up. We’ve been providing the Hometown Hero Credit since 2019 because it was the right thing to do then, and it’s the right thing to do now.

Take the Next Step

Whether you’re a veteran looking to buy your first home or a real estate professional who wants to actually give back, now is the time. The 2026 market is moving fast, and with the VALID Act bringing more eyes to VA loans, you want to make sure you have the 2% credit advantage in your pocket.

Don't leave $21,000 on the table just because nobody told you it was there.

Check your eligibility today or join our movement as a brand ambassador.

Let’s turn that "Thank you for your service" into something you can actually live in.

Brett Stacy

National Director & Founder of the Hometown Hero Credit

A program of Operation T.A.G. (Tangible Act of Gratitude)

501(c)(3) non-profit project of HDCF

Websites: www.OperationTAG.org | www.HometownHeroCredit.com

24-hour Information Line: 760-456-8748

]

]